- Avoid restricted advice firms - always choose 'Whole of Market'

- Poor risk management is the biggest issue for investors

- We assess the actual value in getting quality advice (see example)

- Asset Allocation, fund ratings and rebalancing need to occur regularly

Selecting a financial adviser to manage your investments is a critical decision laden with potential pitfalls that can significantly impact your financial future. However, our analysis of over 30,000 investment portfolios reveals an unsettling truth - only a small proportion of investors are receiving 'gold standard' investment management.

What distinguishes the elite advisers from the rest? What processes and strategies do they employ to maximise returns and safeguard their clients' investments?

This article details the comprehensive, best-practice strategy utilised by top-tier advisers to help maximise investment outcomes for their clients. We examine the key processes and methodologies that distinguish exceptional investment management from the ordinary.

The Pinnacle of Investing

The financial advice and management sector exhibits varying degrees of competency. Top-tier financial advisers cultivate sustainable client relationships through efficient and proven client-centric processes that deliver long-term value.

This article sheds light on the best practice processes adopted by highly competent and successful advisory firms to optimise client efficiencies and investment outcomes.

Investment Management Without Limitations

Financial advisers in the UK can be classified into two main categories: independent or restricted. The key difference lies in the range of products and providers they can recommend.

Independent advisers have the liberty to provide advice on all aspects of financial planning and can choose from the full spectrum of funds available to UK investors. They are not bound to any specific providers or products.

On the other hand, restricted advisers, as the name suggests, can typically only recommend certain types of products or those from a limited number of providers. Their options are restricted in scope.

Some advice firms choose to be restricted to focus on a specific area of financial planning, while others prefer to limit their fund choices to their own range of funds. However, these restricted firms have often faced criticism for 'pushing' their own products, platforms, and investment funds, as well as for earning higher margins by selling their proprietary offerings, thereby limiting their clients' exposure to a narrow range of options.

The largest restricted advice firm in the UK is St. James's Place (SJP), with over £168 billion in client assets under management. SJP and its network of partner advisers only offer their clients access to SJP-branded funds and portfolios, which are regularly criticised for poor performance and substantial fees.

Adding to the complexity, some advice firms are restricted because they choose to specialise in a specific area, such as pension planning or investment planning. Although they cannot advise on other financial matters, they typically have access to the 'whole of market' within their chosen area. For a proportion of investors, such limitations may have little to no impact.

The freedom provided by independent financial advisers and advisers who have access to the 'whole of market' is the unrestricted access they have to better-performing funds and fund managers. While some advisers may not fully utilise this freedom, those who follow best practices and strive to provide top-quality investment management will leverage this liberty to analyse and select the most suitable, top-performing funds for their clients' portfolios, without bias or prejudice.

Efficient Risk Management

Yodelar has analysed thousands of self managed portfolios and we have identified a common theme - one that can have major implications for long term portfolio values. Diversification and risk management of self managed portfolios is often poorly maintained or simply neglected completely.

One of the main advantages of using a quality financial adviser is the expertise and knowledge they can add to investment planning. A good investment adviser will have an understanding of financial markets, and other complex topics that can be difficult for most investors to navigate.

In a study published in the Journal of Financial Counselling and Planning, researchers found that working with a financial advisor can lead to increased financial well-being and reduced stress.

Quantifying The Value of Financial Advice

Vanguard commissioned an independent study to understand what is the value of working with a financial advisor. It found that clients with a financial advisor on average earned about 3% per year more than those without an adviser.

Other studies confirm these findings. For example, the well renowned DALBAR study finds that the DIY investor underperforms by around 3% per year through poor decision making.

What Is Good Investment Advice?

There are a number of key factors that are essential to good investment advice.

Asset Allocation

Asset allocation refers to the percentages of a portfolio invested in various asset classes such as equities, bonds, and cash investments, according to the investor’s financial situation, risk tolerance, and time horizon. It is the most important determinant of the return variability and long term performance of a broadly diversified portfolio.

A sound investment plan begins with an individual’s investment recommendation plan. This outlines financial objectives as well as any other pertinent information such as asset allocation, fund selection, financial contributions, and time horizon. Unfortunately, many neglect this critical effort, in part because it can be very time-consuming, detail-oriented, and tedious. But the financial plan is integral to success; it’s the blueprint for a client’s entire investment strategy and, done well, provides a firm foundation on which all else rests.

Starting with a well-thought-out plan can not only ensure that investors will be in the best position possible to meet their long-term financial goals. Whether the markets have been performing well or poorly, good investment advisers cut through the noise they hear suggesting that if they’re not making changes in their investments, they’re doing something wrong. Almost none of what investors hear pertains to their specific objectives: Market performance and headlines change far more often. Thus, not reacting to the ever-present noise and sticking to the plan can add tremendous value. The process sounds simple but has proven to be very difficult for investors and some advisors.

Asset allocation and diversification are two of the most powerful tools quality advisors use to help their clients achieve their financial goals and manage investment risk. Disciplined advisers who adhere to best practices will engage with their clients at least once a year to assess for changes to their circumstances and to make adjustments where necessary. The implementation of such ‘best practice’ processes helps ensure their clients have a suitable, efficient and robust investment portfolio throughout all stages of their investment lifecycle.

Rebalancing

Given the critical importance of asset allocation, it is equally vital to maintain that allocation over time. As investments generate varying returns, your portfolio is likely to deviate from its target allocation, acquiring new risk-and-return characteristics that may be inconsistent with your original preferences. A portfolio that is overweight in particular sectors or regions becomes more vulnerable to equity market corrections, putting it at risk of larger losses.

Helping investors remain committed to their asset allocation strategy and stay invested increases the probability of achieving their goals. However, the task of rebalancing often presents an emotional challenge for investors. Historically, portfolio rebalancing opportunities have arisen when there has been a wide dispersion between the returns of different asset classes. Whether in bull or bear markets, reallocating assets from the better-performing asset classes to the underperforming ones can feel counterintuitive. But a skilled advisor can provide the discipline to rebalance when it is needed most, which is often when it involves a difficult leap of faith.

Maintaining an appropriate asset allocation is crucial for managing risk and achieving investment goals. While rebalancing may seem counterintuitive, it is a necessary process that helps ensure your portfolio remains aligned with your risk tolerance and investment objectives. A professional advisor can provide the guidance and discipline required to rebalance effectively, even during emotionally challenging market conditions.

Avoiding Emotional Decisions

Because investing evokes emotion, advisors need to help their clients maintain a long-term perspective and a disciplined approach. This can add a large amount of potential value. Most investors are aware of these time-tested principles; the hard part is sticking to them in the best and worst of times. Having emotions isn’t a “rational or irrational investor” issue; it’s a human issue. It’s normal for people to be swayed by the opinions voiced by those considered experts—the talking heads or news headlines that often recommend change. Abandoning a well-planned investment strategy can be costly, and research has shown that some of the most significant challenges are behavioural.

For some investors, factors that affect their wealth are almost as serious as those affecting their health. A quality adviser provides emotional detachment which is one of their most overlooked benefits.

When investors are tempted to abandon the markets because performance has been temporarily poor, advisers can remind them of the plan they created before emotions were involved. The trust a good adviser creates can be crucial in helping investors meet their financial goals.

Advisors can act as emotional circuit breakers by circumventing clients’ tendencies to make emotional decisions in changing markets. In the process, they may prevent significant wealth destruction and add value. A single such intervention could more than offset years of advisory fees.

Complex Planning Requirement

When faced with complex financial planning requirements, the value of high quality financial advice becomes paramount. For instance, it can be extremely challenging for an individual to independently arrange and map out their own phased retirement plan (if that is the most suitable option) as they approach retirement, or to implement the most effective strategies to protect their assets from Inheritance Tax.

Specialised financial advice is precisely that: highly specialised. Moreover, many aspects of financial planning are interconnected, meaning that the advice required in one area could have implications for another.

In such intricate scenarios, working with a high quality financial advisor can prove invaluable. These professionals possess the expertise and experience to navigate complex financial situations. They can develop tailored strategies that address your unique circumstances and align with your long-term objectives, providing guidance and support throughout the process.

Find an Adviser Who Can Identify Top Quality Investments

One of the most neglected aspects of investment advice is related to fund performance. In order for investment advisers to identify which funds outperform their peers and then apply these funds to efficient investment portfolios, they must have the ability to identify, analyse and regularly review the performance and overall quality of each fund. Top advice firms will show clients their process for analysing funds, and often share this information with clients by incorporating processes that filter funds based on set performance criteria.

One system applied by some quality firms to track and manage fund performance is referred to as the traffic light system. This system uses a 3-tiered fund grading model that promotes a pragmatic investment approach and helps to avoid poor investment decisions.

The Investment Traffic Light System

This system categorises funds based on their relative performance compared to others in the same sector, using a traffic light analogy.

Green Rating

Funds that have primarily maintained a level of performance exceeding 75% of their peers within the same sector over a 1, 3, and 5-year period are typically assigned a green rating. These funds are viewed as top performers and have represented excellent investment opportunities. When constructing a portfolio, green-rated funds are predominantly considered.

Amber Rating

Funds that were previously rated green but have recently experienced a decline in performance compared to other funds within the same sector are assigned an amber rating. These funds remain within the portfolio but are carefully monitored, typically over a 3-6 month period, to identify whether their performance has improved, remained stagnant, or declined further in comparison to the sector average. If the fund's performance improves to a level better than 75% of competing funds in the same sector, it regains a green rating. If it remains stagnant, it will continue to receive an amber classification for up to 6 months. However, if no improvement is observed during this period, it will receive a red rating.

Red Rating

A red rating signifies that action is required. It may involve removing the fund from the portfolio and replacing it with a suitable green-rated fund. Funds are moved to a red rating if they continue to drop in sector rankings over a 3-6 month period or if they fail to improve six months after receiving an amber rating.

By utilising this Investment Traffic Light System, financial advisors can proactively monitor the performance of the funds within their clients' portfolios and take appropriate actions to ensure that the investments remain aligned with the desired risk and return objectives.

Successful Investing Requires Patience

It is important to understand that successful investing is not reliant on chasing or reacting to current trends, but from maintaining a strategically risk balanced portfolio of high quality funds over a medium to long term investment horizon.

Throughout history, many global regions and markets have experienced sharp performance swings without a clear catalyst - such as the tech stock crash in early 2000. Many investors had overloaded in North American funds with a high weighting in technology stocks in the late 1990s only to find themselves overexposed when the bubble burst, leading to painful losses.

Yet even when markets fall, if a portfolio contains high quality funds that are managed by quality fund managers, losses will recover provided investors remain in the market over a sufficient time frame. Investors who make decisions based on short term trends will be negatively impacted and will experience significant losses for 2 reasons:

(1) Overloading increases the pain when that market experiences a sharp downturn as an overweight portfolio will lose a greater percentage of its value.

(2) Investors who overload into trending asset classes are more likely to abandon the asset class they were over-reliant on if it does drop in value. This locks in any losses and relinquishes the potential gains from a market recovery

The guidance and the implementation of a strategy from a quality adviser can remove the desire to chase performance or overloading into one asset class and keep your investments on the right track.

Investing Is About The Destination, Not The Journey

Successful investing involves diversification, patience and time. In the table below we show how remaining invested during all market cycles since the start of the century can result in profitable gains. For this example we reviewed recent bear markets in the S&P 500 Index.

As the table above demonstrates, even if you had the worst possible timing - meaning you invested £10,000 on each of the six peak days immediately before a bear market began - your investments would have lost value initially. However, they would have always recovered in time. The above table shows an investment of £60,000 over the course of the periods highlighted would have grown to £195,995 by the end of 2022.

Even if you had invested at the worst-possible times, the amount you invested would have more than quadrupled in time. Throughout history markets have always rebounded from previous downturns 100% of the time. Overloading into the best performing asset classes of the moment makes such returns practically impossible.

In short, for long-term investors who have the time horizon to weather ups and downs, the length of time you’re in the market matters far more than the point in time at which you begin investing.

Quality Advice Can Help Maximise Investment Potential

While the key factors for good investment advice can add value to any investment portfolio there are a number of additional factors that most advisers don't utilise, factors that can add even more value to investors.

A limited number of advisers possess extensive expertise in fund and fund manager performance, crucial areas that, if carefully assessed and strategically utilised, can greatly enhance the construction and management of a high-performing fund portfolio, ultimately adding substantial value.

These skilled advisors excel in constructing and managing portfolios tailored to their clients' risk tolerance and financial goals. However, as with any industry, there are professionals who excel in their craft and those who fall short. The challenge in the financial sector lies in the difficulty for clients to discern the level of expertise of their advisor until they entrust them with their investments.

When entrusting your portfolio to a financial advisor, it's crucial to partner with someone who possesses in-depth, research-driven knowledge of fund performance. While some advisors excel in expertise and understanding of fund selection, it's important to note that fund performance is not a regulated aspect of financial planning. As a result, many advisors may lack the necessary expertise in evaluating the quality of funds they recommend.

Top-tier advice and investment management firms possess a deep understanding of fund and fund manager performance, allowing them to pinpoint optimal choices and construct high-performing portfolios efficiently. This expertise is what sets the best advice firms apart from the rest.

Leading The Way For Investors

The development of Yodelar Investment portfolios come from years of research and analysis that include the consistent assessment of more than 100 fund managers, tens of thousands of funds and more than 30,000 investment portfolios.

Our research continues to identify that a small proportion of funds and fund managers consistently delivered top performance, with more than 90% of the portfolios we review containing funds that continually underdeliver. This research has enabled us to identify efficient processes and top-quality investments which we have utilised to create 10 strategically balanced, risk-rated portfolios that are built using only the top funds within each asset class and offer investors phenomenal potential for growth.

Yodelar provides a regulated whole of market advice and information service that is changing the way investors think.

Book a no obligation call with our team today and find out how we can help you grow your wealth efficiently.

Finding The Best Partner To Manage Your Investments

Many new potential clients that come to Yodelar are unhappy with their existing returns, previous adviser, or the results they have had from self managing their investments.

We often hear from investors that they are shopping around prior to making a decision. That is great, and always welcome but the biggest issue (and we see this a lot) is that they do not know what they are shopping for. The result is they often end up going with the best salesman, but not the best adviser.

For your convenience, we have created a list of key considerations that can help when it comes to choosing the best adviser to manage your investments.

1. Whole of market access to all funds/managers (not restricted)

2. Clear defined risk models

3. Can demonstrate the performance of the funds recommended

4. Have knowledge of the investment sectors and performance within each

5. Have a clear, transparent and competitive charging structure

6. Clearly defined service structure, for example, one full review per annum, regular rebalances etc

7. UK based with defined response times and service standards

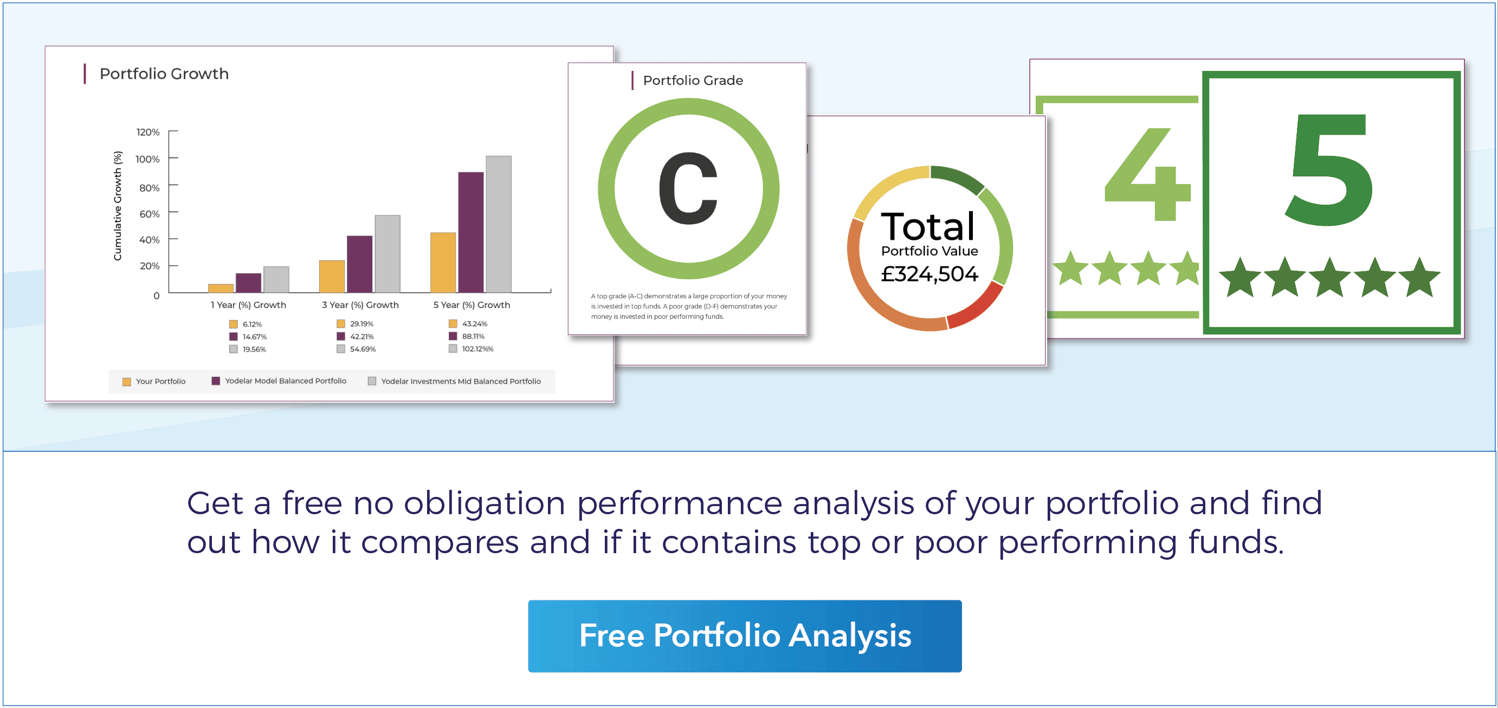

How Efficient Is Your Portfolio?

For years, Yodelar has analysed the performance and quality rating of portfolios for thousands of UK investors. Our extensive analysis has uncovered that over 90% of investors hold portfolios containing inefficiencies that stunt growth potential, resulting in many UK investors to miss out on enhanced portfolio growth.

Inefficient investing can have adverse long-term consequences, making it crucial to identify and correct any portfolio deficiencies.

Our industry leading portfolio analysis service enables investors to find out how their portfolio compares to a similar risk-profile portfolio constructed with top-performing funds. This unique tool provides measurable ratings that offer complete transparency into the quality of individual fund choices and the overall portfolio's competitiveness.

By leveraging our portfolio review feature, investors gain detailed insights into the performance of their investments and can identify whether their current approach is optimally positioned for growth.

Key Benefits Include:

- Evaluate the performance of each fund

- See where each fund ranks within its sector over 1, 3, and 5 years

- Find out how each funds performance rating between 1 to 5-stars

- Determine the proportion allocated to top, mediocre, or underperforming funds

- Compare portfolio growth against model portfolios built with consistent top performing funds

- Get an overall portfolio performance grade from A to F