Warren Buffet says that markets are a device to transfer wealth from the impatient to the patient. Poor diversification, not setting your objectives and time horizons, using a restricted advice model, over paying, emotional reactions, and misjudging risk exposure are all part of the investment process we see on a daily basis that clients get wrong.

In this article we address the 10 common mistakes investors make which have the potential to cause significant damage to your portfolio's long term value.

Topics Covered In This Article

In this article we review the 10 risks that can cause damage to your investments and identify what you can do to avoid popular errors.

1. Underestimating the time horizon of your assets

2. Misjudging The Risk Exposure Needed To Meet Investment Objectives

3. Failing To Properly Diversify

4. Overreacting to negative cycles

5. Emotional decision making

6. Restricting investment choices

7. Impatience

8. Overconfidence in Your Investing Skills

9. Paying too much in fees

10. Making uninformed decisions

Understanding the pitfalls and making more informed decisions could make all the difference.

Introduction

Investing will always require an element of risk but for investors to have a successful investment journey there are a number of mistakes they need to avoid and options they need to consider.

If an investment strategy is managed efficiently, even after a negative market cycle, you can still expect to meet your medium to long term goals. The real challenges are not from fluctuations in investment cycles but in the creation, delivery and management of each investment strategy.

-

1. Underestimating The Time Horizon for Your Assets

-

How long do you think you’ll live? How long do you think your spouse will live? Usually, investors are far too conservative in estimating the length of their lives, and that can be a problem when planning their financial futures.

As the effectiveness of medical treatment, nutrition and standards of living improve, many people now live longer than they imagine they will. As a result, they fail to plan financially for a longer life with the time horizons for their investments often falling short.

Another major mistake for investors is setting their time horizon at the time they aim to retire, which can result in cash flow problems in later life and missed opportunities for greater growth due to more conservative strategies as they get closer to their retirement date, and also during retirement.

For example, a 55 year old planning to retire at 65 may believe they have an investment time horizon of 10 years - despite reasonably expecting to live another 25 years. They might place a big part of their portfolio in fixed interest or cash to reduce short-term volatility, an asset allocation that may not generate enough growth to support future cash flows, if their time horizon proves longer than they perceived. Forgoing the long-term growth a higher equities allocation could yield can increase the risk of portfolio depletion. Those who realise this too late may have limited options to reposition their portfolio for cash flow in old age

Investors run the risk of depleting their funds long before their lives are over. It is important to have a sound financial strategy that will provide financial stability and meet income needs throughout one’s life. Sound financial planning is equally important for those whose goals are to grow their assets to pass an inheritance on to loved ones and family members who survive them. If this is the case, then the family members' investing time horizon should be considered also; this may be substantially longer than their own. In either case, a realistic life expectancy time horizon is vitally important.

-

2. Misjudging The Risk Exposure Needed To Meet Investment Objectives

Aligning your portfolio strategy with your objectives is a critical factor in determining long-term investing success. This may sound obvious, but many investors actually employ strategies that work against their objectives.

A common error investors make is misjudging risk. Generally speaking, the longer the investment time horizon, the more risk one is able to take on. Typically, however, many investors do not take enough risk. They focus on short-term volatility rather than on the long-term probability of achieving their objectives. The result tends to be portfolios that underperform against their goals.

Investors must manage the tension between long-run objectives and the risks of unacceptable losses over the course of the investment life cycle. Meeting long-term investment objectives can involve the risk of experiencing larger-than-expected losses in the interim. Conversely, taking too little risk can result in getting a good night’s sleep but eventually waking to the reality that long-run objectives have been compromised.

For example, some persistently load their portfolios with cash and fixed-term bonds, afraid that equities will drop in the short-term. These often barely generate a return that is above the rate of inflation, thus reducing the odds of achieving a longer-term goal of growth—especially if withdrawals are also anticipated.

At the other end of the spectrum those with short investment time horizon objectives are often overly exposed to risk, which creates a danger of asset loss during a short-term period of volatility. This can put their entire financial future in jeopardy.

Aligning investment objectives with the most appropriate risk strategy and time horizon is a crucial element of investing that is unfortunately often misunderstood.

-

3. Failing To Properly Diversify

To ignore diversification is to ignore risk. A portfolio that does not diversify is much more likely to fail in meeting any long term investment objectives.

The only way to create a portfolio that has the potential to provide appropriate levels of risk and return in various market scenarios is adequate diversification across asset classes and of course across fund manager brands.. Often investors think they can maximise returns by taking a large investment exposure in one security or sector. But when the market moves against such a concentrated position, it can be disastrous. Too much diversification and too many exposures can also affect performance. The best course of action is to find a balance.

While diversification could mean that you forgo superior upside in one shock event, the long-term benefit of the improved risk reduction outweighs any perceived short-term relative loss. It’s this delicate balance that necessitates an in-depth analysis of each asset class, each portfolio those assets support, and each possible future scenario.

Source: RLAM, Refinitiv DataStream as at September 2022.

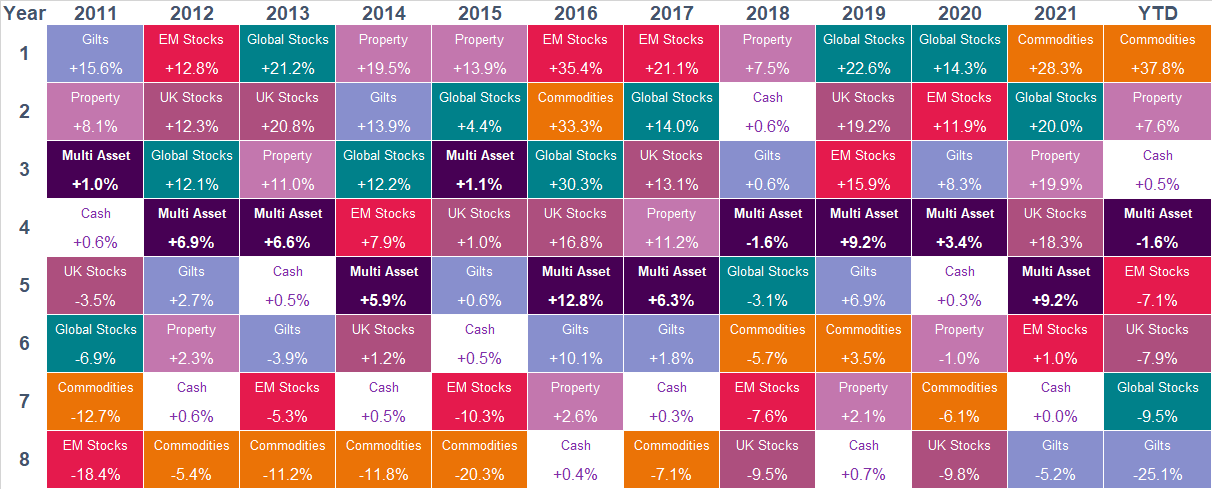

No single equity style, sector, country or region outperforms all others all of the time. Global diversification spreads risk amongst countries and currencies to offset the risk of investing in just one region or country. As such, globally-diversified portfolios are vital to long-term investment success.

Spreading your risk across various countries shields investors from country-specific conflicts and regulations. In this way, if one country struggles economically due to regional issues, your portfolio will feel that it affects less.

Article: The Important of Portfolio Diversification

-

4. Overreacting To Negative Cycles

Do not let your emotions dictate your investment decisions. It’s important not to be scared by a falling market. Recall the reasons why you picked your investments in the first place, and refer back to this when you are feeling spooked.

Considering in advance how you may react to a market correction could help prevent you from making any expensive mistakes, and selling shares at a loss instead of waiting for an upturn in the market.

Remember that corrections are going to occur and are an inevitable part of investing. They might be unsettling, but holding your nerve could be the best way to protect your investments.

No investment strategy will outperform in every reporting period and every type of market condition. As much as we may not like it, we can expect some periods of underperformance.

Important point: If the quality of your portfolio was low during previous market cycles it is reasonable to assume it will be poor going forward, so in such circumstances reviewing your portfolio and its underlying fund performance would be beneficial in helping to identify whether or not alternative options need to be considered.

-

5. Emotional Decision Making

Stay strategic

If you have a well-diversified portfolio, then it’s more important than ever to stay the course. You have a strategy in place that reflects your risk tolerance and time horizon, so stay committed. However, if you reacted and sold in a previous market decline or have not implemented a strategic asset allocation, then now is the time to have a discussion about your investment options.

Stay calm

The first thing to do when volatility is high is to stay calm. It can be easy to work yourself up into a panic when stocks are falling, but this won’t help you. Making calm, rational decisions is one of the keys to long-term investing success. Remember – you haven’t actually lost money until you sell. Stocks will recover, as they have historically done 100% of times in the past.

Stay focused

No one knows how severe any market turbulence will be or what the market will do next. It could be over quickly or linger for a while. But no matter what lies ahead, proper diversification and perseverance over the long term are what’s most important.

-

6. Restricting Investment Choices

-

Restricted advice can mean restricted fund choices. The investment portfolios of fund management firms that offer a restricted advice service will typically only ever use their own small range of funds in the portfolios they invest their clients' money in. This approach significantly limits the number of quality options that are available to investors which can be detrimental to meeting performance objectives as no one fund management firm has top performing fund options across all core asset classes.

What is restricted advice? - It was not until 2014 that the Financial Conduct Authority issued a definitive fact sheet outlining what ‘independent’ and ‘restricted’ advice actually means in practice, and what is expected of advisers using these labels.

The distinction between the 2 has often divided opinion. Some are of the view that restricted advice does not impact on the quality of the advice consumers receive whereas others have argued that restricted firms often go down this route so that they can sell their own investment products, or those of their parent company, for their own gains instead of that of the consumer / client investor.

Why does it matter?

Independent Financial Advisers (IFA’s) are able to consider and recommend all types of retail investment products that could meet your needs and objectives. They are able to consider products from all firms across the market, in order to give unbiased and unrestricted advice.

Financial advisers with a ‘restricted’ status cannot provide advice on ‘whole of market’ products but there are differing degrees of restrictions that ‘restricted’ advisers work to. For example, there are advisers who hold a restricted status because they won’t advise their clients on specialist products such as VCT’s (Venture Capital Trusts) or ETF’s (Exchange Traded Funds). Such limitations may have little to no impact on a proportion of investors.

When Financial advice companies choose to become restricted in order to ‘push’ their own products, platforms and investment funds, that ‘restricted’ advice can be detrimental to the consumer. Such practices mean firms can earn bigger margins from selling their own products, and their clients are only exposed to a small range of products that might not be best suited to their needs - while often being more expensive.

We believe that by having access to funds across the whole market and with no allegiance to any fund manager, investors can benefit from an unrestrictive approach to investing that allows the freedom to make fund choices based on quality and suitability, which we believe is important in obtaining high level portfolio efficiency and performance.

-

7. Impatience

Warren Buffett said: “The stock market is a device which transfers money from the impatient to the patient.”

Patience will reward investors. In fact, it is viewed as the most important principle for successful investors.

Many people believe that knowing when to buy and when to sell is the secret of successful investing. The truth is that no one knows with certainty when markets will rise or fall. Trying to time the market is very seldom successful. It’s far better to use time to your advantage. The sooner you can start investing, and the longer you can invest for, the more likely it is for you to achieve your financial goals, regardless of any short-term blips. Of course, the strategy and quality of funds are crucial to maximising potential gains but even the best investments will have periods of underperformance that will test the patience of investors.

If we look at any quality fund with a long term history and break the funds performance into 6 months, 1 year or even 3 year segments, they will show periods of underperformance. Periods where they lost sizeable chucks of value and tested the resolve of their investors. But when looked at over a longer period almost all will have delivered net growth.

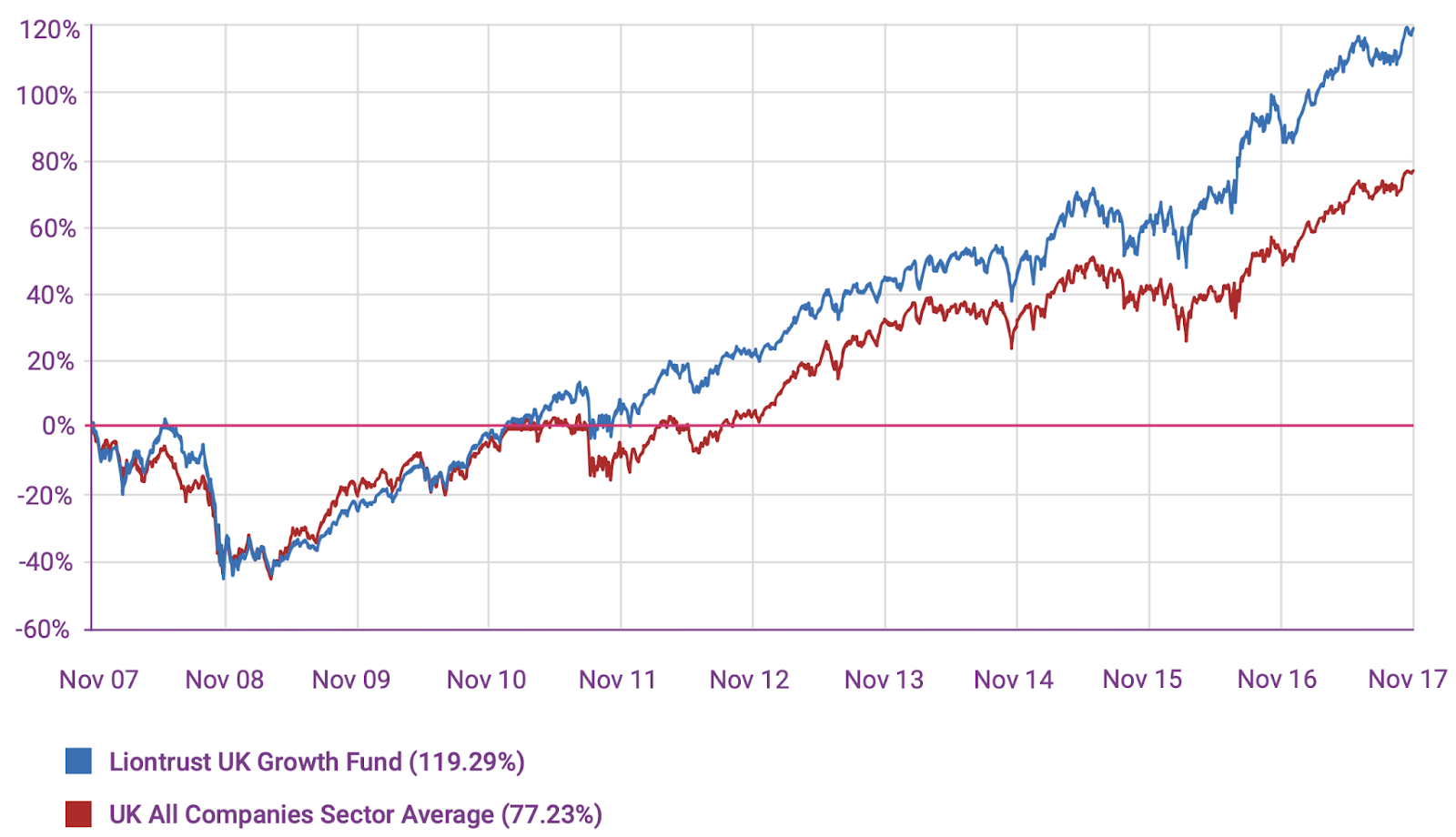

An example of this can be seen with the Liontrust UK Growth fund, which is a popular UK equity fund with a history of strong performance in its sector. But as the table below shows this isn’t always visible.

If we focus on the 1 year period between October 2007 and October 2008, which was the period of the ‘subprime mortgage crisis’, the fund returned negative growth of -45.72%, which was below the average for the period and resulted in a large number of worried and impatient investors to cut their losses and abandon the fund.

But when looking at the funds performance over a longer period, as per the above table, the picture changes considerably. In the 10 years period from October 2007 to October 2017 the fund returned growth of 119.29%, which was 64% higher than the sector average.

Although 1 year may seem a long time to some investors, particularly during a volatile period, it really isn’t. As mentioned earlier, confidence comes from understanding that your investments are being managed efficiently and following best practice processes. For such investors, periods of underperformance are easier to accept as they have confidence that in the longer term the quality of their investments will deliver. A lack of understanding and confidence can result in investors selling off funds that have experienced a period of under performance, which is often much more costly in the longer term.

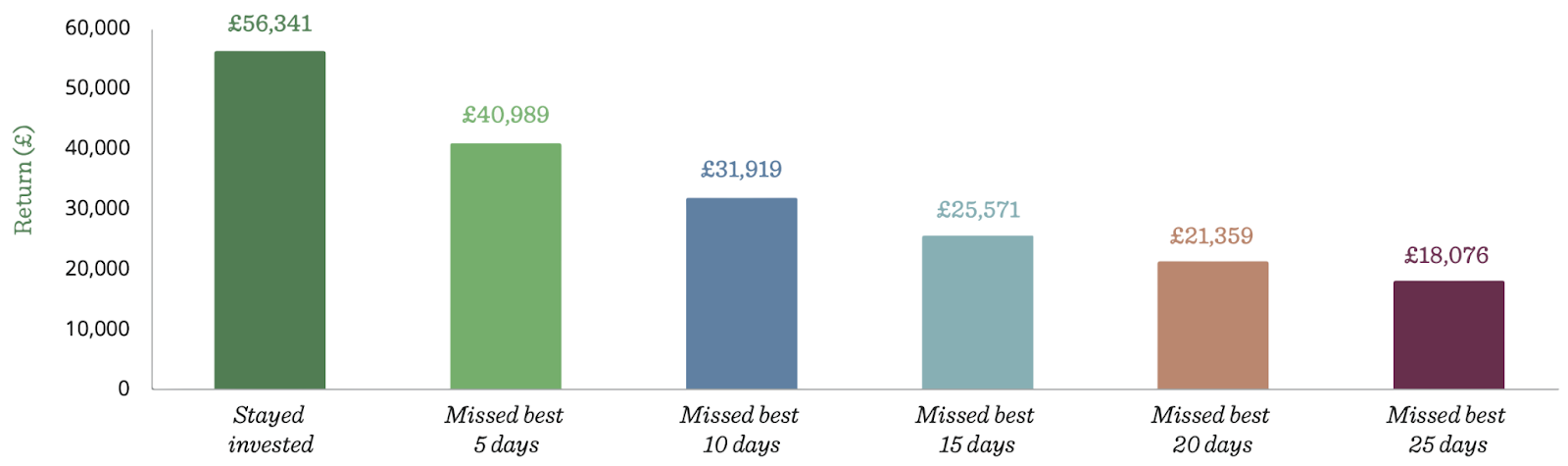

The table below shows just how costly it can be to miss out on the best days in the 20 year period between 31st December 2001 and 31st December 2021. It shows that if you had stayed invested in global equities over the entire period, you could have had a potential return that was three times greater than that of an investor who missed the best 25 days during the same period, based on both of you investing £10,000.

-

8. Overconfidence in Your Investing Skills

When investing personal assets, it’s natural to experience emotional fluctuation as you watch the ups and downs of the markets each day. After all, you're dealing with your financial future. The typical result is that a slew of cognitive biases come into play, clouding people’s judgement and hampering the ability to make rational, impartial decisions.

Many investors, for example, will focus on their successes and try to forget the mistakes they’ve made, consistently confirming their personal views rather than maintaining objectivity. One particular shortcoming is an innate tendency toward overconfidence. We naturally put up barriers that allow us to forget the mistakes we’ve made in the past. Similarly, we tend to focus on the successful investments we’ve made—which makes us overly confident. This may lead to taking on excessive portfolio risks. No one is immune to these biases. That’s why it’s vital to create an environment for investing that is detached from emotion, one that relies on data and impartial analysis to make the right decisions for your financial future.

Investment risk, portfolio diversification, and portfolio realignment are 3 important elements of investment that can be managed ineffectively by some self investors.

For example, our research team recently analysed a portfolio for an investor through our free portfolio analysis service, who classified themselves having a mid level investment risk strategy. Our analysis identified recent performance that was comparatively high, which reaffirmed their confidence in their investment ability. However, when one of our senior advisers discussed the analysis with the investor they were able to identify that the portfolio of funds were limited to one asset class and industry sector. The portfolio performance is therefore reliant entirely on this sector doing well. Naturally, when it does well the rewards will reflect that sector's growth but when it declines, which all markets and sectors inevitably experience, then the entire portfolio value will drop resulting in concentrated losses. As such, the portfolio did not assume a mid level risk strategy as intended but rather a very high level of risk.

-

9. Paying Too Much in Fees

The returns generated by investors are often undermined by fees they pay. For a smaller investor, running a portfolio can result in very high percentage annual charges. Even in the modern age of “low cost” internet accounts, these charges can make the difference between outperforming and underperforming the market.

This can happen in several ways. If an investor is self-managing a portfolio with a “low cost” platform they will pay a set fee per trade and often an annual administration charge too. Unless the amount traded is relatively high, the set fee can be an unexpectedly large percentage figure. This can be thought of as an “upfront fee”. Since it is well established that investors tend to have high levels of trading activity, this compounding of an upfront charge can be very damaging to resultant performance.

Investors who prefer not to self-manage may hire an advisor to build a portfolio of funds that, in some cases, can cost 3% or more per annum when you incorporate adviser charges, the underlying fund management charges, and portfolio turnover costs. Such high fund fees can dash any hopes of long-term outperformance.

It is always imperative to ascertain the manner in which service providers, be they advisers, funds or dealing platforms, derive their fees in order to understand their true motives. Your wealth manager should have profit incentives that align their goals very closely with your own.

-

10. Uninformed Decision Making

Often investment decisions such as which advice firm to entrust in managing your money or which funds to invest in are made without a true understanding as to their quality. Investing is too important to make decisions that are not backed up by research.

There are currently more than 100 different fund management firms in the UK offering investors access to thousands of investment funds. To add further complexity, new funds enter the marketplace each month adding to the thousands of funds that are currently available. So how can you make more informed investment decisions?.

The Yodelar InvestorHub™ portal has been developed to enable investors to identify the funds and fund managers that have consistently outperformed their peers, as well as highlighting the inefficiencies of many funds and investment portfolios.

Through our research we have developed a platform that provides a number of unique features to help investors make more informed investment decisions and improve outcomes.

A Balanced Approach To Investing

Investing, like many aspects of life, isn't always straightforward with many pitfalls that need to be navigated, some of the main ones we have highlighted in this article.

The fact is, the investors who reach their objectives efficiently are typically those who have a disciplined and pragmatic approach to investing, and follow a structured, long term strategy. When this is followed better outcomes can be achieved. By understanding and taking action to avoid the traps featured in this report investors can add strength to their investments and improve outcomes.

Article: 8 Reasons To Invest With Yodelar

Leading The Way For Investors

At Yodelar our team of investment experts can help to navigate the challenges of investing and help achieve your investment goals efficiently and effectively.

The development of our portfolios comes from years of research and analysis that included the consistent assessment of more than 100 fund managers, tens of thousands of funds and more than 30,000 investment portfolios.

Our research continues to identify that a small proportion of funds and fund managers consistently delivered top performance, with more than 90% of the portfolios we review containing funds that continually underdeliver.

This research has enabled us to identify efficient processes and top-quality investments which we have utilised to create a core growth focused range and a low cost ESG range of strategically balanced, risk-rated portfolios that are built using only the top funds within each asset class and offer investors phenomenal potential for growth.

Yodelar provides an advice and information service that is changing the way investors think.

Book a no obligation call with our team today and find out how we can help you growth your wealth efficiently.