- A recent study carried out by Vanguard found that investors with a financial adviser on average earned about 3% per year more than those without an adviser.

- Research from the Centre for Economic Policy Research (CEPR) found that ‘Investors who delegate portfolio management to a financial advisor achieve on average greater returns, lower risk, lower probabilities of losses and of substantial losses, and greater diversification through investments in equity funds.’

- A report by the Financial Conduct Authority (FCA) analysed the behaviour of self investors identifying 3 primary traits that can lead to poor investment choices.

- The FCA also reports that four in ten self investors do not view ‘losing some money’ as a potential risk of investing.

The value of investment advice has always been a topic that has divided opinion among investors. Some see great value in advice service whereas others see it as an unnecessary expense. The value of investment advice is also now challenged by convenient, lower cost self investor platforms which have pushed more investors towards managing their own portfolios. Yet despite the challenges posed by self managed platforms and the perceptions of high advice costs, research from Vanguard shows that investment advice on average increases portfolio values by 3% per year.

Investment advice and its associated costs, more often than not, has proven to be the best option for investors to make with even the regulator voicing concerns about the risks of self managed investing.

In this report we look at why financial advice is often the best option for investors, we detail the benefits of advice and explain why the FCA have concerns about the dangers of self investing, particularly in recent years as these numbers rise.

Why you might need a Financial Adviser

There are many reasons for taking financial advice. You might be looking for a better return on your investments, wanting pension advice to ensure you have security in retirement or simply trying to avoid financial decisions you may later regret.

However, think carefully about what type of help you need, can afford and would add value. Not everybody needs full-blown professional financial advice.

Stephen Kavanagh, chief executive at Chase de Vere, an independent financial adviser (IFA), says: “For many people, their basic financial planning should be paying off debts, building cash savings, paying off their mortgage, joining their company pension scheme and understanding the protection benefits provided by their employer.”

However, individuals with larger amounts of savings and investments or higher earnings can benefit from taking financial advice. Significant events in your life, such as inheriting money, having a child, getting divorced, or deciding when to take pension benefits are just some of the scenarios in which a professional opinion could prove a wise investment.

Independent or restricted advice?

The difference between independent and restricted advice is significant and can have a huge impact on investment outcomes.

Advisers fall into two broad categories — independent or restricted. An independent adviser can recommend their pick of retail investment products from across the market. In essence, they have access to all available funds from all fund management brands, across all asset classes. As they have no restrictions they can in theory select, build and maintain a portfolio that contains the most suitable funds for their clients.

Restricted advisers can usually only recommend certain types of products or those from a limited number of providers. Most of the larger and better-known investment houses give restricted advice. These include St James’s Place, Hargreaves Lansdown and Tilney as placing client money into their own fund range has obvious benefits to their business.

As an example of how restricted advice limits fund choice, St. James’s Place, the UK’s largest restricted advice network, limits their clients who wish to invest in an ISA or general investment account to a selection of just 36 SJP branded funds. In contrast, an independent adviser has a choice of over 3,000 funds, providing them with the opportunity to identify and invest in the best funds for their clients.

“Many advisers choose to be restricted because it means they can sell their own products and investment funds. This is understandable from their perspective, but it isn’t such a good idea for clients if their products are expensive and of poor value,” Chase de Vere CEO Stephen Kavanagh.

Improve Performance Through Research

Through investor focused tools such as Investor hub™, investors have access to highly educational and informative fund performance information that will increase fund knowledge and help self investors improve fund choices and portfolio quality. As such, the need for financial advice when it comes to performance is not what it once was. But it is not just performance where advisers add value, but more importantly - managing a clients diversification and risk management. These are crucial to long term investment success. Over the past several years, Yodelar has analysed thousands of self managed portfolios and identified a common theme - one that can have major implications for long term portfolio values. Diversification and risk management of self managed portfolios is often poorly maintained or simply neglected completely.

What Is Good Investment Advice?

There are a number of key factors that are essential to good investment advice.

Asset Allocation

Asset allocation refers to the percentages of a portfolio invested in various asset classes such as equities, bonds, and cash investments, according to the investor’s financial situation, risk tolerance, and time horizon. It is the most important determinant of the return variability and long term performance of a broadly diversified portfolio.

A sound investment plan begins with an individual’s investment recommendation plan. This outlines financial objectives as well as any other pertinent information such as asset allocation, fund selection, financial contributions, and time horizon. Unfortunately, many ignore this critical effort, in part because it can be very time-consuming, detail-oriented, and tedious. But the financial plan is integral to success; it’s the blueprint for a client’s entire investment strategy and, done well, provides a firm foundation on which all else rests.

Starting with a well-thought-out plan can not only ensure that investors will be in the best position possible to meet their long-term financial goals but can also form the basis for future behavioural coaching. Whether the markets have been performing well or poorly, good investment advisers cut through the noise they hear suggesting that if they’re not making changes in their investments, they’re doing something wrong. Almost none of what investors hear pertains to their specific objectives: Market performance and headlines change far more often. Thus, not reacting to the ever-present noise and sticking to the plan can add tremendous value. The process sounds simple but has proven to be very difficult for investors and some advisors.

Asset allocation and diversification are two of the most powerful tools advisors can use to help their clients achieve their financial goals and manage investment risk.

Rebalancing

Given the importance of selecting an asset allocation, it’s also vital to maintain that allocation. As investments produce different returns over time, the portfolio likely drifts from its target allocation, acquiring new risk-and-return characteristics that may be inconsistent with your original preferences. A portfolio overweight to particular sectors or regions is more vulnerable to equity market corrections, putting it at risk of larger losses.

Helping investors stay committed to their asset allocation strategy and remain invested increases the probability of meeting their goals. But the task of rebalancing is often an emotional challenge for investors. Historically, portfolio rebalancing opportunities have occurred when there has been a wide dispersion between the returns of different asset classes. Whether in bull or bear markets, reallocating assets from the better performing asset classes to the worse-performing ones feels counterintuitive. But a good advisor can provide the discipline to rebalance when it is needed most, which is often when it involves a very uncomfortable leap of faith.

Advisors who can systematically direct investor cash flows into the most underweighted asset class or rebalance to the most appropriate boundary are likely to reduce rebalancing costs and thereby increase the returns their clients keep.

Behavioural Coaching

Because investing evokes emotion, advisors need to help their clients maintain a long-term perspective and a disciplined approach. This can add a large amount of potential value. Most investors are aware of these time-tested principles; the hard part is sticking to them in the best and worst of times. Having emotions isn’t a “rational or irrational investor” issue; it’s a human issue. It’s normal for people to be swayed by the opinions voiced by those considered experts—the talking heads or news headlines that often recommend change. Abandoning a well-planned investment strategy can be costly, and research has shown that some of the most significant challenges are behavioural.

For some investors, factors that affect their wealth are almost as serious as those affecting their health. A quality adviser provides emotional detachment which is one of their most overlooked benefits.

When investors are tempted to abandon the markets because performance has been temporarily poor, advisers can remind them of the plan they created before emotions were involved. The trust a good adviser creates can be crucial in helping investors meet their financial goals.

Advisors can act as emotional circuit breakers by circumventing clients’ tendencies to make emotional decisions in changing markets. In the process, they may prevent significant wealth destruction and add value. A single such intervention could more than offset years of advisory fees.

Complex Planning Requirements

When complex financial planning is required, the value of financial advice can prove vital. For example, it would be very difficult for an individual to arrange and map out their own phased retirement plan (if this is their best option) when they come to retire, or for an individual to put in place the best measures to protect their assets from Inheritance Tax.

Specialist financial advice is just that: specialised! And because so much of the financial planning requirement is connected or inter-connected then the advice required in one area could knock onto another.

The FCA’s Concerns For Self Managed investors

FCA report - https://www.fca.org.uk/publication/research/understanding-self-directed-investors.pdf

Recent research by the FCA identified the personality types who make up the self-directed investor market.

-

1. Self-directed investors’ investment journeys are complex and highly personalised, driven by underlying motivations, personality, confidence, knowledge and external factors (e.g. life stage, financial situation, lifestyle).

Three self-investor types have been identified, based on motivation, attitude and approaches to investing:

Having a Go: newer or less experienced self-directed investors who lack extensive knowledge about investing and are keen to do it on their own. They often look to learn through doing and adopt shortcuts to decision making which can include going with ‘hyped’ options they have heard a lot about, or viewing mainstream, big name brands as a short-cut to what they believe are ‘safe’ investing (e.g. investing in tech companies).

Thinking it Through: more experienced self-directed investors, or those with a professional or academic background in maths, finance, economics or business. These self-directed investors feel they have high levels of knowledge and are very confident in their abilities (although this can be misplaced in reality). They often use shortcuts built up from experience and background knowledge – for example, seeing certain data patterns as indicating a ‘safe choice’.

The Gambler: behaviourally very separate, this group tends to see investing on a similar level to ‘betting’. These self-directed investors are particularly attracted to short-term high-risk, high-return options.

-

2. Emotional and social motivations are often key in driving self-directed investing, either alone or in addition to more functional motivations.

Motivators have differing relative importance across different archetypes.

- ‘Having a Go’ tends to be motivated by a combination of functional (making money, working harder) and emotional factors (challenge, novelty).

- Thinking it Through are often more motivated by social factors, such as feeling like ‘an investor’, being able to prove their know-how and talking to others.

- The Gambler are usually more emotionally motivated by the thrill and excitement and are looking to ‘beat the game’ and ‘win’.

-

3. Regardless of which archetype they represent, self-directed investors, particularly those investing in high-risk, high-return types, tend to have a high degree of confidence and claimed knowledge. However, the reality of their behaviours and beliefs around investing indicate that this can be misplaced.

In particular, there is a striking lack of awareness and/or genuine belief in the risk of investing, with over four in ten (45%) not viewing ‘losing some money’ as a potential risk of investing – despite the presence of disclaimer warnings.

Additionally, most have high confidence in their abilities, although in reality strategies largely rely on an investment opportunity ‘not feeling right’ or looking unprofessional. Included in the research were self-directed investors that had been victims of scams and frauds who noted these had looked legitimate and professional.

Online ethnography with self-directed investors also showed that many generally do not have a systematic or strategic approach to investing when it is being observed, despite this being how they tend to describe their approach. Gut instinct is hugely important in decision making across archetypes, as is the use of short-cuts and rules of thumb to circumvent more extensive learning and research.

The FCA’s findings show the different traits of self investors and just how overexposed each of these can leave investors.

Also, research from the Centre for Economic Policy Research (CEPR) found that ‘Investors who delegate portfolio management to a financial advisor achieve on average greater returns, lower risk, lower probabilities of losses and of substantial losses, and greater diversification through investments in equity funds.’

Quantifying The Value of Financial Advice

Vanguard recently commissioned an independent study to understand what is the value of working with a financial advisor. It found that clients with a financial advisor on average earned about 3% per year more than those without an adviser.

Other studies confirm these findings. For example, the well renowned DALBAR study finds that the DIY investor underperforms by around 3% per year through poor decision making.

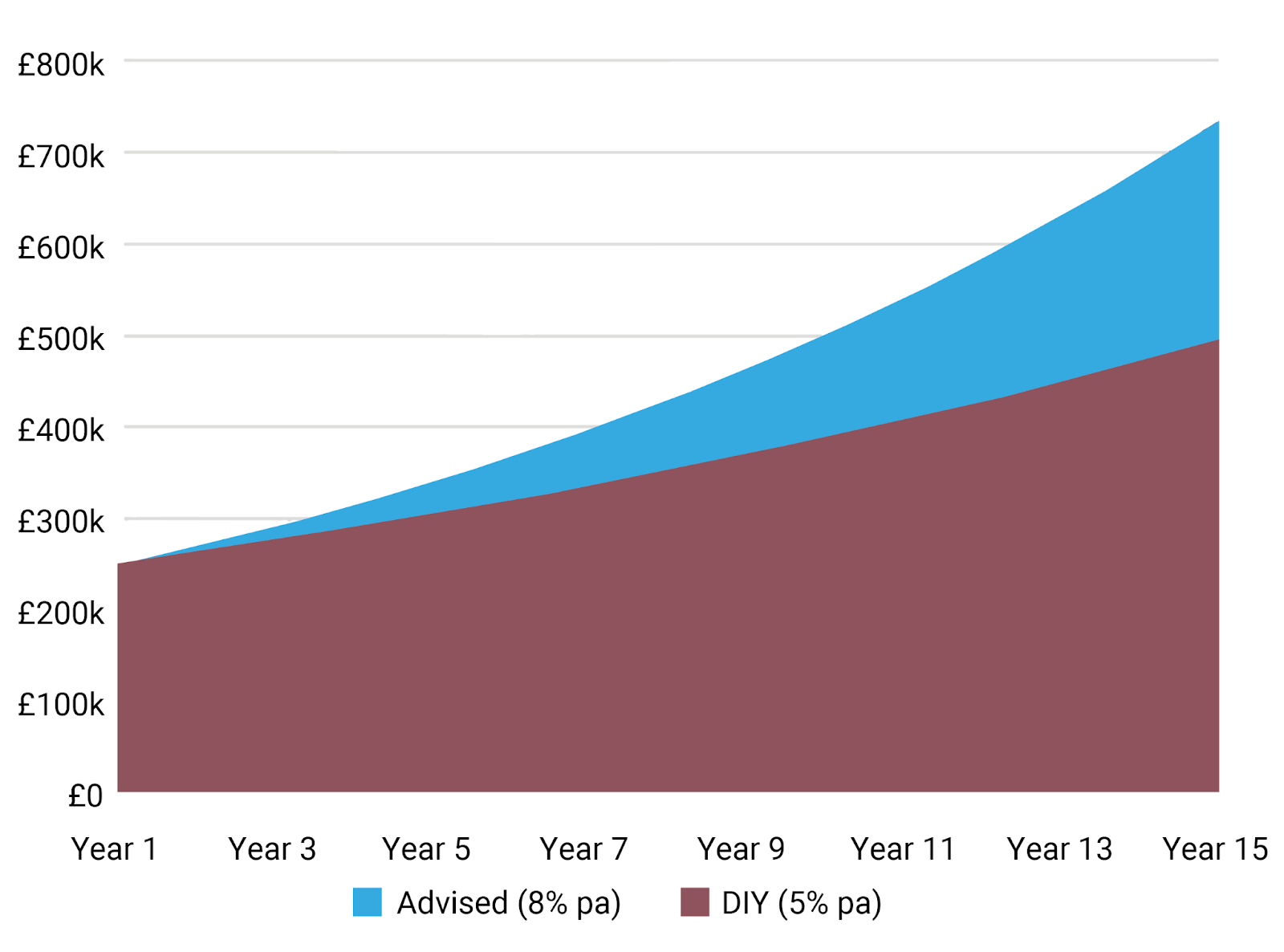

How much does 3% per year add up to?

Whilst 3% per year might not sound like much, over time, it can be significant.

Let’s assume that you have £250,000 in investments. In an average year, these investments might grow by 5% per year. Over a period of 15 years, your investments would grow to £495,000.

If you work with a financial advisor and achieve the extra 3% per year, the same investment would grow an additional £240,000 to £734,000.

Both studies show this isn’t about finding a better investment to generate an extra 3% per year. It’s about avoiding costly mistakes, like selling at the wrong time, taking too much risk or paying too much tax.

Good Advisers Take Care of Risk

Over the past several years, Yodelar has analysed thousands of self managed portfolios and we have identified a common theme - one that can have major implications for long term portfolio values. Diversification and risk management of self managed portfolios is often poorly maintained or simply neglected completely.

One of the main advantages of using a quality financial adviser is the expertise and knowledge they can add to investment planning. A good investment adviser will have an understanding of financial markets, and other complex topics that can be difficult for the average person to navigate.

In a study published in the Journal of Financial Counseling and Planning, researchers found that working with a financial advisor can lead to increased financial well-being and reduced stress.

Quality Advice Can Help Maximise Investment Potential

While the key factors for good investment advice can add value to any investment portfolio there are a number of additional factors that most advisers don't utilise, factors that can add even more value to investors.

Although financial advisers can add sizeable value to investors over the course of their investment horizon, only a relatively small proportion have a high level knowledge of fund and fund manager performance. 2 areas that if measured and used effectively to implement and maintain a top performing portfolio of funds, can add significant additional value.

Such advisers are able to build and manage efficient portfolios suitable to their clients’ risk profile and overall objectives. But like any industry, there are those who are good at what they do, and there are those who are not. The main difference in the financial sector is that it is very difficult for a client to know whether their adviser has the expertise until they take the chance and invest with them.

Quality advice and portfolio management firms understand fund and fund manager performance and are able to use this knowledge to identify the best options and build efficient, top performing portfolios. It is this process that distinguishes the top advice firms from the rest.

Leading The Way For Investors

The development of our portfolios come from years of research and analysis that include the consistent assessment of more than 100 fund managers, tens of thousands of funds and more than 30,000 investment portfolios. Our research continues to identify that a small proportion of funds and fund managers consistently delivered top performance, with more than 90% of the portfolios we review containing funds that continually underdeliver. This research has enabled us to identify efficient processes and top-quality investments which we have utilised to create 10 strategically balanced, risk-rated portfolios that are built using only the top funds within each asset class and offer investors phenomenal potential for growth.

Yodelar provides a regulated whole of market advice and information service that is changing the way investors think.

Book a no obligation call with our team today and find out how we can help you grow your wealth efficiently.