St. James’s Place have continually faced questions over their advice, product and service charges, with high upfront fees taking away large chunks of an investment that in some cases takes several years to recoup. But it is their exit penalties that lie in wait for those who wish to move their money out of SJP pension or bond products that are the most contentious.

It isn’t just their exit fees that can prove costly to those who wish to move away from SJP products. SJPs restrictive policies can mean those with a Trust administered by SJP, are unable to leave this trust without incurring a taxable event that could cost the beneficiary as much as 40% of the value of the assets in their trust.

What implications do these exit charges have on SJP fund performance and why can moving a trust out of SJP products cause a fallout that can have significant financial consequences?

Fees & More Fees

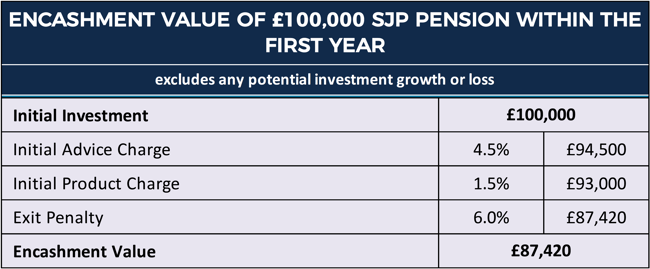

St James's Place charges start with the initial advice fee charged to their range of pension and bond products. This amounts to a significant 4.5% of your initial investment.

Alongside the initial advice charge is an initial product charge which costs a further 1.5% of the value of your initial investment. Therefore, a St. James’s Place pension or bond product will cost a combined 6% of the amount you initially invest in upfront fees alone.

In addition to the charges for the advice and product SJP also charge clients for managing and maintaining the underlying investments. These fees differ from fund to fund, and therefore their total can vary.

To provide an indication as to what these charges can be the SJP Balanced Income pension portfolio with a value of £100,000 would be charged approximately £548 for management and maintenance costs each year.

On top of that, there is also what SJP refer to as an annual product management charge, which is more commonly known as an exit penalty. Investors in an SJP retirement or investment bond products will be charged an additional 6% of the value of each fund they are invested in should they wish to cash in or transfer their account within the first year of setting it up. This penalty reduces by 1% for each year no money is withdrawn. So, a 6% penalty charge in year 1 would reduce to 1% in year 6.

If you invested £100,000 in a St James's Place pension product and wished to withdraw entirely from this product in the first year, without factoring in any potential investment growth or losses, you would only receive back £88,360 due to SJPs initial charges and exit penalties.

Such extensive upfront charges and exit penalties have led to accusations that St James’s Place and their charging policies are designed to both maximise initial fee income as well as secure longterm revenue by using high exit penalties to lock investors in.

Trustee's Beware!

It isn’t exclusive to their pension and bond products where St James’s Place have come under fire for their perceived use of penalties for customers who wish to go elsewhere.

In recent weeks we have spoken to several trustees who manage trusts that were set up through St. James’s Place. These trustees questioned the ethics of SJPs policies and highlighted the potentially significant financial penalties they would face if they decided to move assets of the trust elsewhere.

What Is A Trust?

A trust is simply an agreement, usually in writing, which defines the relationship between individuals and assets. For example, a property is often held in trust for the benefit of specific individuals, known as beneficiaries. The person who provides the assets is called the settlor, and he or she expresses their wishes in the trust document.

Trustees are usually appointed (in addition to the settlor) and administer the trust in accordance with those wishes and relevant trust law. (The FCA does not regulate trusts, but they are legal agreements bound by the Trustee Act 2000.)

Generally, the assets transferred into the trust, and any benefits arising from it, will have to be managed for the benefit of the beneficiaries - the trustees are responsible legally to the trust and the beneficiaries.

To facilitate the creation of a trust, St. James’s Place have their own legal document that allows ‘the settlor’ to open a trust and place their assets into various investment or savings products that sit within the trust.

One of the primary benefits for setting up a trust is to protect assets against Inheritance tax. The standard Inheritance tax rate is currently 40% on assets that are above £325,000. But each year the trust is in place the IHT liability reduces, and after seven years the tax liability is zero, which is of significant benefit for the beneficiaries.

One of the key priorities of the trustee is to get a suitable plan in place that helps to maximise the assets efficiently. Typically, trustee's seek financial advice to proportion the assets within a range of investment products that match their aptitude to risk and best fit their investment objectives. Should a fund or investment product underperform, they have the freedom to move these assets to other potentially better-suited products.

Trustee Complaints

After reading our recent St James's Place review a number of Trustees contacted Yodelar to voice their concerns regarding the restrictions placed on the trust to which they are responsible to.

Unlike a trust set up by many other providers, SJP will only allow their own products to be held within the trust even if the trustee deems that not to be in the best interests of the beneficiaries.

If the trustee's of a Trust believe it is in the best interest of the beneficiaries to move the assets to another provider, SJP would close the trust instead of facilitating the wishes of the trustee, potentially exposing assets to inheritance and capital gains tax.

Trustee's who are responsible for a trust with SJP have no choice other than to stay with them and keep the assets in funds they no longer deem in the best interests of the beneficiaries.

One of the legal obligations of trustees is to invest the trust fund efficiently and in the beneficiaries’ best interests. Being restricted and unable to move funds outside of SJP, may in effect make them liable under the Trustee Act, on the basis that they are not acting in the best interests of the beneficiaries.

Consider Your Options

St James's Place Charges and expensive model have been widely documented yet as a company they continue to grow, and as the UK's largest wealth manager they now boast assets under management in excess of £95.6 billion.

In their most recent annual report, SJP report strong client retention of 96%. But when you take into account their substantial client numbers, the 4% who left and took their money elsewhere equated to more than 25,000 investors.

According to SJP 97% of their clients say they would recommend St. James’s Place, indicating that the majority of their investors are happy to pay high charges and accept their penalties and restrictive policies.

As one of the most expensive wealth management companies in the UK with restrictive products and policies, those considering moving to St. James’s Place should take time to fully consider the implications of such a move and take into account the largely better performing and lower priced investment products/propositions available elsewhere.